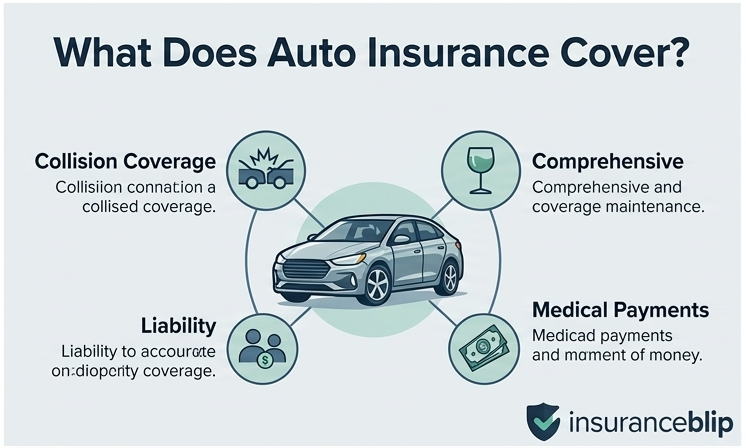

Auto insurance is a contract between you and an insurance company that provides financial protection when something goes wrong with your vehicle, whether that’s an accident, theft, weather damage, or a liability claim from another driver. In exchange for paying a regular premium, your insurer agrees to cover certain costs up to the limits defined in your policy.

It’s one of the most common types of insurance in the United States, and for good reason: a single accident can result in thousands of dollars in vehicle repairs, medical bills, and legal expenses. Auto insurance exists to protect you from bearing those costs alone.

If you want to estimate what coverage might cost you, use our Auto Insurance Cost Calculator.